| Insurance IP

Bulletin

An Information Bulletin on

Intellectual Property activities in the insurance

industry

A Publication of - Tom Bakos Consulting, Inc. and Markets, Patents and Alliances, LLC |

April 15, 2007 VOL: 2007.2 |

||

| Adobe pdf version | Give us FEEDBACK | ADD ME to e-mail Distribution |

| Printer Friendly version | Ask a QUESTION | REMOVE ME from e-mail Distribution |

| Publisher Contacts

Tom Bakos Consulting, Inc.

Tom Bakos: (970) 626-3049 tbakos@BakosEnterprises.com Markets, Patents and Alliances, LLC Mark Nowotarski: (203) 975-7678 MNowotarski@MarketsandPatents.com

Building on Prior Art Question: I have found some journal articles that provide useful information for improving my invention. If I incorporate what these articles teach into my patent application, will that cause me problems later on?Disclaimer:The answer below is a discussion of typical

practices and is not to be construed as legal advice of any kind. Readers are

encouraged to consult with qualified counsel to answer their personal legal

questions. Answer: Usually not, as long as you cite the articles to the patent office. In fact, quite the opposite may be true. The more you can build upon the prior work of others, the better your invention will be and hence the stronger your patent application will be. The only other choice would be to ignore what these articles teach and that wouldn’t be too smart. After all, it’s out there and if the information will improve your invention you would be foolish not to use it to do just that. There is a common reluctance among inventors to incorporate what others have taught into their own patent applications. The concern is this will somehow dilute the notability of their inventions and their patents won’t get allowed. They may be right in the very rare cases where someone has previously taught exactly what the invention is. In the vast majority of cases, however, an inventor needs to adapt the earlier teachings of others in order to use them in their invention. These adaptations become the foundation of a patent. It has been our experience that patent examiners feel much more comfortable saying “yes” to a patent that acknowledges the contributions of others and builds upon them. The prior teachings of others help to highlight the particularly novel features of an inventor’s invention. The

other thing to remember is that the ultimate goal of an inventor is to see

the invention adopted as widely as possible. It makes no sense to turn a blind

eye on prior teachings that could improve an invention for fear that an

inventor might not get a patent.

The end goal, after all, is commercial success, not simply getting

a patent. Webinar Notice: How to Speed Up Your Patent ApplicationOur Mark Nowotarski will be presenting a free webinar entitled “How to Speed up your Patent Application”. The webinar will be held on April 30, 2007 at 12 noon to 1 pm Eastern daylight time. Attendees will receive practical guidance on steps they can take to potentially cut the time it gets their patents in half. The webinar is targeted at start-ups and independent inventors. The webinar is sponsored by the Connecticut Technology Council. For more information and registration, go to http://www.ct.org/Events/ViewSchedule.asp?pass=1&ID=2279, or call Kathy Slater at 860 289 0878 x20 Meeting Notice: How to get a Financial Service

Patent in

|

This issue we provide some insight into the things an inventor ought to consider in putting a sales package together for his or her invention. Unfortunately, good ideas don’t sell themselves. Pay attention to the business success stories you read about – almost all, that involved some grand new idea, appeared headed for failure in the beginning. Patience and perseverance are required to move the status quo as described in Getting to First Base. In

our Patent Q/A we address a question

inventors have often asked regarding how best to deal with prior art or

articles related to an invention in a patent application. The

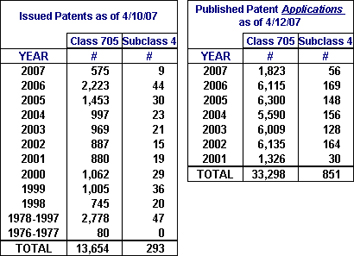

Statistics section updates the current status of issued

Our mission is to provide our readers with useful information on how intellectual property in the insurance industry can be and is being protected – primarily through the use of patents. We will provide a forum in which insurance IP leaders can share the challenges they have faced and the solutions they have developed for incorporating patents into their corporate culture. Please use the FEEDBACK link above to provide us with your comments or suggestions. Use QUESTIONS for any inquiries. To be added to the Insurance IP Bulletin e-mail distribution list, click on ADD ME. To be removed from our distribution list, click on REMOVE ME.

Thanks, FEATURE ARTICLE Getting

to First Base

By: Tom Bakos, FSA, MAAA & Mark Nowotarski, Patent Agent, MPA, LLC Mark: Well Tom, spring is in the air. The birds are singing. The flowers are blooming. A young man’s fancy turns to … Tom: Baseball? Mark: Exactly. And you know what I love the most about baseball – getting to first base. It’s the hardest thing for me to accomplish but once I’m there, I can see my way to home. Tom: Something similar can be said about many of our clients. Whether they are independent inventors or employees of major corporations, at some point, they have to “get to first base” with an investor who has the resources necessary to turn an insurance innovation into a commercial insurance product. That investor may be the management the company the inventor works for, it might be an angel investor who will fund a start-up company, or it might be an alliance partner who will license the invention. In any event, getting an investor to say “yes” to sponsoring the commercial development of an invention is like getting to first base in baseball. It can be hard, but it’s the first step towards home. Mark: I like the analogy. Can you offer any advice to our readers on how to get to first base with a potential investor based on your experience in the insurance industry? Tom: Well, I think there are three very important things to consider:

You always have to start with the status quo. Insurers are not oblivious to innovation. Obviously, it happens in the insurance industry. But, not many practice it. Most follow the demonstrated success of the few who do. Mark: So most insurance carriers, brokers, insurance marketing companies, and the like that have funds available for new product development see themselves primarily as “fast followers” and don’t really want to try anything first. Most organizations find the talk of innovation and paradigm shifts inspiring and most insurance companies want to be known as innovative problem solvers, but the status quo is a heavy weight. Tom: That’s because the status quo works, even if imperfectly, whereas something brand new might not work at all. Insurers have experience in what they are doing and in what they see the rest of the industry doing. Contrary to what those outside the industry may think, insurance companies do not take or accept risk, they understand and manage risk. Mark: I ran into exactly that situation when I spoke recently to the head of new business development of a major insurance carrier at a meeting on insurance innovation. His job was specifically to bring new ideas into the company. I mentioned to him that I had a client with a new idea that he might be interested in. He replied “Great, just as long as it’s not XXX insurance”. I asked him, “Why not XXX insurance?” He said that they had just talked to an inventor about that new type of insurance, but his company wasn’t interested because they had no experience with it. “So”, I said, “You are only interested in new ideas that you already have experience with?” “Yes.”, he replied, “That’s what we are looking for.” Tom: Now we’re to my second point: “Don’t call it new, call it better”. An inventor with a patented new product innovation has, by definition, something that is new, useful, and not obvious. But, in order to have success in selling it to an investor, the inventor has to package it in terms that the investor is most familiar with. By describing an innovation in terms of how it is “better” than an existing product or process, the inventor creates a link or implied transition between old and new. Some of the familiarity of the old is implicitly transferred to the new. That makes investors more comfortable about their financial risk in product development. Mark: That’s quite a paradigm shift for inventors. Often inventors have just spent considerable effort convincing the patent office just how new their inventions are. Now you’re saying that when these same inventors bring their patented inventions to potential investors, they have to emphasize how similar their ideas are to what the investors are already investing in. Is that it? Tom: Exactly. In a sense, what an inventor needs to sell is not so much a “new” as it is a “better-old”. I think a new product or process idea is best presented in terms of how it can replace an existing product or process or how it can do something that the old process doesn’t do at all. Start with the status quo. Insurers understand the status quo and will more readily acknowledge the problems in the status quo once an inventor with a better idea points them to a potential solution. A recognized problem in the status quo coupled with an innovative, workable solution is a hit. It plays on the dissatisfaction everyone seems to have with the status quo while staying away from the fear of the new and unknown. Mark: Which brings us to your final point, “Don’t waste your time on rejection”. My dad was a salesman and he had a great expression for this: Good salesmanship starts with a NO. In other words, a swing and a miss is part of the game. Rejection, disappointment, and frustration are part of any sales process. The objective is to learn from the rejection and transform it into a stepping stone to success. Tom: That’s right. Both you and the potential investor want the same thing, success. If you listen with an open mind to a rejection, you will hear the investor telling you exactly what he or she wants to invest in. If you adjust your offering accordingly, you might be able to stretch that base hit into a home run. |